Ask any market observer, professional or casual, and they will tell you that concentration is the defining challenge in financial investment today and, as a consequence, a challenge for wealth management and portfolio construction. Whether measured by the dominance of a single country, a single sector, or a shrinking roster of listed companies, markets are increasingly driven by a narrow set of forces. The consequence is not academic: diversification, the most venerable and effective risk management tool in finance, has become harder to achieve.

The numbers are revealing. The popular “Magnificent Seven”[1] now carry a combined market capitalization of roughly $22 trillion and account for close to a third of the S&P 500, a concentration level without modern precedent. Over three decades, the number of domestically listed U.S. companies has quietly shrunk from a peak of 8,090 in 1996 to trough of roughly 4,572 by 2023, a 43% decline, even as the market’s aggregate value nearly tripled. If one invests in a capitalization-weighted U.S. benchmark today one is making a concentrated bet on a handful of companies, one sector, and one economic narrative, more than at any point in modern market history. Unsurprisingly, investors are questioning whether passive, benchmark-driven portfolios can still deliver on that old promise of diversified exposure to the economy at large, across diverse sectors, i.e., with breadth and depth.

The wealth management industry’s answer has been swift and increasingly uniform for institutional investors first, and retail ones recently: go private! If the domestic public opportunity set has narrowed, the reasoning goes, look beyond it entirely, i.e., look into private equity, private credit, and other illiquid corners.[2] While the conclusion may have value, it is not, however, the only one, far from it. There are many more attractive and massive opportunities for both diversification and return opportunities. I.e., before going private, investors should first consider going global.

Indeed, and especially in the USA, the diversification debate almost always starts with an simplified assumption: that the relevant investment universe is the domestic market, not realizing that different countries, regions, etc. have different markets compositions, thus offering exactly the diversification benefits sough after. In addition, and while the U.S. market has narrowed, the global one has quietly undergone its own revolution. Investors today can reach virtually every country, every asset class, every sector, every recognized factor, every major commodity, and hundreds of specialized themes — some 190-plus countries, roughly 60,000 listed companies, and $152 trillion of equity market capitalization, most of it a click away through a single, liquid, low-cost wrapper. Global equity markets alone added more than $23 trillion in value in 2025 — an 18.5% gain in a single year, and a sum roughly equal to the entire global ETF industry today. The investment universe has not shrunk. It has become dramatically larger, and it keeps growing faster than any single domestic market, with remarkable breadth and depth, by any measure.

To be fair, the U.S. listings story isn’t really about markets shrinking; it’s about where the growth has moved. Research into the “U.S. listing gap”[3] shows the divergence starkly: as American exchanges lost roughly half their listed companies between 1996 and 2012, the rest of the world added tens of thousands of new ones, climbing from about 30,700 to over 55,000 today. An investor who defines the opportunity set as “the U.S. market” is, by construction, fishing in a shrinking and increasingly concentrated pond, however large that pond’s aggregate value may have become. An investor who defines it as “the global market” is fishing in a pond that has been expanding continuously for more than three decades.

The most common objection, of course, is that investing globally is considerably more demanding. It requires broader market knowledge, greater analytical capabilities, and a deeper understanding of countries, sectors, factors, currencies and asset classes. That is certainly a concern. Yet, what is more difficult to understand, however, is why these very challenges are often used to justify an even more demanding alternative: allocating capital to private assets, i.e., an investment universe that is inherently illiquid, less transparent, more difficult to value, operationally more complex and generally far more expensive.

The ETFs revolution … global investment made easy and affordable.

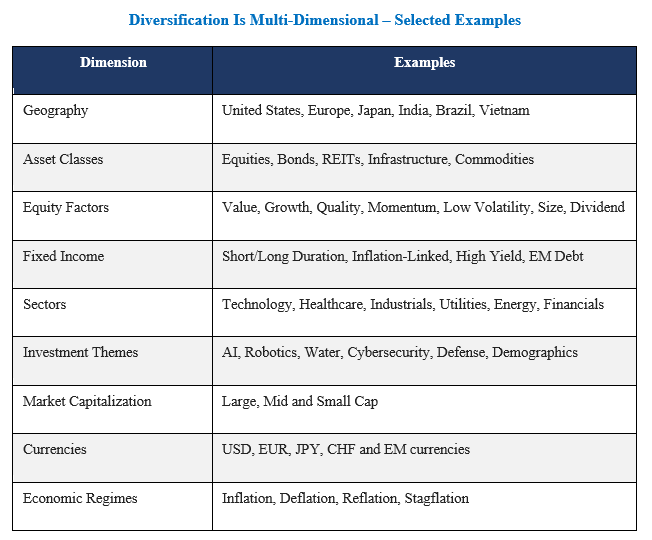

True diversification, of course, means more than adding asset classes. It means expanding the number of independent return sources in a portfolio: geography, sector, style, factor, currency, economic regime. For many years, the principal objection to global diversification was not conceptual but practical. Exploiting a truly global opportunity set required specialist managers, multiple mandates, considerable operational complexity and substantial costs. In many respects, global investing remained the preserve of large institutional investors. This argument, however, has largely disappeared.

Today, investors can gain efficient exposure to virtually every country, sector, factor, asset class, commodity, currency and investment theme through transparent, liquid and inexpensive investment vehicles. More than 16,600 ETFs, traded across 86 exchanges in 66 countries and managing a record $23 trillion in assets, have fundamentally changed the economics of global investing. The vehicle itself is almost incidental.

The product has also matured. Active ETFs, barely a rounding error a decade ago, have grown from roughly 412 funds in 2020 to more than 1,500 by the end of 2024, and now account for the majority of new launches. Increasingly, they promise investors exposure not only to global markets and systematic factors but also, allegedly, to active management skills, incidentally one of the traditional selling points of private equity and other alternative investments. What matters is that the barriers to implementing genuinely global portfolios have largely vanished. In other words, accessing global markets is, in short, no longer the problem, selection is.

The implication is straightforward. If the objective is broader diversification, more specialized exposures or even access to active management, investors today enjoy an extraordinary range of public-market solutions that are transparent, liquid and inexpensive. Private assets should therefore be viewed as an additional dimension of diversification, not as the inevitable next step once domestic markets become more concentrated.

Conclusion

The dilemma facing wealth management, then, is real. Some, albeit bigger markets have grown more concentrated and more uniformly directional, and investors are right to want broader sources of diversification, and not only for risk management’s sake but also return opportunities. The popular response has been to embrace private assets on the promise of more return, less volatility, and genuine diversification from public markets. The trouble is that private markets’ delivery on all three counts has been faltering of late … structurally, perhaps.[4] Private assets are best understood as an additional dimension of diversification, not an all-weather solution.

This extraordinary expansion of the global opportunity set compounded by innovative vehicles has fundamentally changed the investment problem. For decades, the challenge was access. Today, it is selection, and, increasingly, portfolio construction, model and customized! The question is no longer whether investors have enough opportunities. It is whether they can identify the most attractive ones (i.e., less complex, liquid, cheap … and performing!) and combine them into portfolios that are genuinely diversified and aligned with their objectives.

Before wading into increasingly illiquid and expensive private assets, investors should first ask whether they have fully exploited the extraordinary breadth already available across global public markets. That breadth has never been greater, and the tools to access it have never been more powerful, more transparent or more affordable. Technology and financial innovation have democratized access. Artificial intelligence is now democratizing selection. The future of diversification does not begin by leaving public markets. Perhaps it simply begins by leaving domestic ones.

Simon E. Nocera

Lumen Global Investments LLC

San Francisco — California

July 2026

[1]Apple, Microsoft, Tesla, Amazon, Nvidia, Alphabet, and Meta.

[2]As one industry veteran quipped, “there are now more private equity shops in the U.S. than McDonald’s restaurants.”

[3]Doidge, Karolyi & Stulz, “The U.S. Listing Gap” (NBER Working Paper 21181); World Federation of Exchanges, 2025/2026 statistics; ETFGI, May 2026.

[4]Nocera, Simon E., The Private Equity Illusion: Revisiting Risks, Returns, and Realities (July 12, 2025). Available at SSRN: https://ssrn.com/abstract=5400925