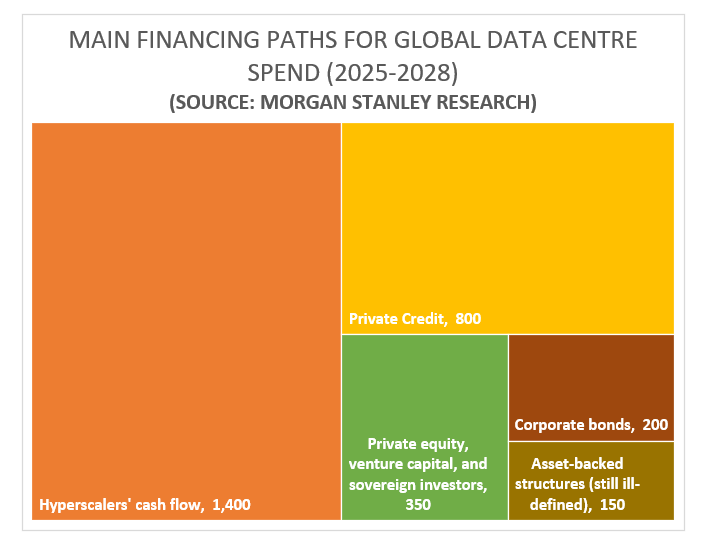

The scale of the coming AI infrastructure buildout is unprecedented. Global data-center capacity is projected to expand sixfold by 2030, implying capital expenditures of roughly $3 trillion by 2028. About half of that may be funded internally by hyperscalers’ own cash flow (Google, Microsoft, etc.), with credit markets expected to fill the remainder. The indicative funding arithmetic estimated by Morgan Stanley runs as follows:

Momentum and Monetization

The Capex wave is already rolling. Investments, which totaled about $125 billion in 2023, are on track for $200 billion in 2024, and may exceed $300 billion in 2025, all largely financed from internal cash generation by the major cloud platforms.

The reason: Morgan Stanley analysts project that Gen-AI-related revenues could exceed $1 trillion by 2028, up from roughly $45 billion in 2024, with variable margins at around 70 percent. However, a timing mismatch looms between investment and monetization: much of the cash is being deployed ahead of visible revenue capture, creating a capital-funding gap.

The Funding Debate

The bullish view argues that private capital will eagerly bridge this gap. As the argument goes, the characteristics of AI infrastructure—long-term, high-yielding, and complex—fit the playbook of private credit, infrastructure funds, and alternative investors. Reportedly, the narrative holds that this cycle differs from the early-2000s telecom bubble because funding is now distributed across many balance sheets and investors, not concentrated in a few over-leveraged corporates, i.e., risk is spread out across many holders. Moreover, hyperscalers today boast stronger credit profiles, substantial free cash flow, strong balance sheets, and a tangible revenue trajectory for AI services.

The skeptical view, however, points out that the arithmetic strains credibility. The entire global high-yield market is about $1.4 trillion—so an incremental $800 billion from private credit would be extraordinary. Similarly, hyperscalers allocating $300–400 billion per year would approach half of the entire S&P 500’s current total Capex (≈ $950 billion).

Moreover, roughly $1.3 trillion of the planned outlays target physical infrastructure—land, buildings, cooling, and connectivity—while the remainder will purchase GPUs and hardware that depreciate by 30 percent per year. That raises legitimate questions about securitization and collateral value in asset-backed structures of this scale, especially for an asset that loses 30-35% of its value every year (i.e., GPU/chips).

The Missing Piece: Energy

What is striking is what’s not included in most forecasts: power infrastructure.

If, as estimated, half of new data centers will be U.S.-based, the country would require an additional 45 gigawatts of generation capacity—about 10 percent of current national output, equivalent to 23 Hoover Dams or 45 power stations. The U.S. grid’s installed capacity stands near 1.25 terawatts; 45 GW would equal half the entire nuclear fleet or more than all of California’s current generation. How such capacity materializes by 2028 remains uncertain.

Capital, Competition, and Complacency

Optimists cite roughly $4 trillion in “dry powder” available from private credit globally. Yet competition is intensifying given emerging players such as DeepSeek, and given the broader commoditization of computing power that could pressure margins, there could be an echo of the telco bandwidth glut two decades ago. High capital intensity, rapid obsolescence, and potential data-center overcapacity add to the risk.

When the most enthusiastic projections envision a 1,900 percent increase in AI data-center spending by 2028—an order of magnitude above the telecom Capex boom, or 10x, it’s hard to dismiss the possibility of excess and misallocation. With the US market clearly driven by the AI revolution, and with the US Market now being roughly 60 percent of the global market, there is no question that the “exuberance” of this Capex arithmetic warrants a cautious stance of most global portfolio … and efficient diversification across themes, styles, and factors!

Simon Nocera

Lumen Global Investment LLC

October 2025