The Mighty Dollar, Again!

“The US Dollar is our currency, but it’s your problem.” ~ John Connally, Secretary of the Treasury of President R. Nixon, G10 Meeting, Rome, Italy 1971

This is an update of Simon’s original popular article on “The Mighty Dollar” - a timely discussion of what it means for the recent decline of USD.

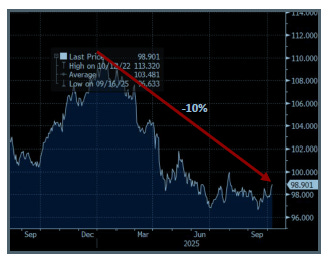

Using the DXY index, the dollar has declined by roughly 10% since the new Administration came in. Matched against the current global and U.S. backdrop, the cacophony about the dollar’s “demise” is getting louder and louder. While further weakness is possible, the decline so far is neither unusual nor alarming and is warranted by fundamentals. Indeed, on a REER (Real Effective Exchange Rate) basis, the dollar was overvalued by roughly that amount (around 10%). Any further decline from here would bring the currency into “cheap” territory. In short, there is no reason—now as many times before—to think that the recent decline is a precursor of the long-time expected demise of the dollar with a further massive downside.

Chart 1: USD decline since new Trump’s Administration (Source: Bloomberg)

A common and more “reasonable” narrative compares the current backdrop for the dollar today to 2000 to 2004. Back then, the dollar fell ~30% on an index (DXY) basis and ~20% on a REER basis amid a rare convergence of headwinds (a “perfect storm”):

Introduction of the Euro, expected to dethrone the dollar

The dotcom bust, triggering capital outflows from U.S. equities

September 11

Fed cuts from 6.5% (2001) to 1% (2003)

The twin US deficits (fiscal and current account)

A dollar that was roughly 20% overvalued (on index measures)

To be sure, the ~30% drop was essentially the mirror image of the late-1990s surge, i.e., it was an unwinding of exuberant capital flows and policy normalization globally. Then, like today, the Mighty Dollar survived!

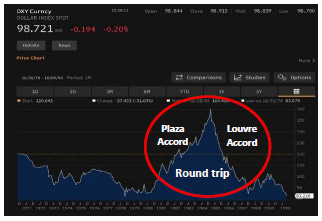

The other major decline (~40%) was the Plaza Accord in 1985 (after the dollar had almost doubled the prior year), followed by the Louvre Accord in 1987 to stabilize FX. Plaza 1985 → dollar down; Louvre 1987 → stabilization. In the end, another “roundtrip” in the value of the dollar.

Chart 2: Dollar’s “roundtrip” from 1985 to 1987 (Source: Bloomberg)

The point is that in every episode, calls for the dollar’s demise were simply shortsighted. The reason: one must distinguish between the Role of the Dollar in global finance and economy from the Value of the Dollar. The Role sets sturdy guardrails “supporting” the dollar and making it the most unique currency in the world. The “market” level or value of the dollar then moves those guardrails based on normal economic/financial drivers. While valuation can justify moves up or down, the guardrails are the institutional uses of the dollar in the global system—beyond which the currency rarely strays. And here is why:

Monetary & Financial Role

58% of global FX reserves are held in USD

88% of global FX transactions involve USD

~50% of global trade is invoiced in USD

~50% of global cross-border loans are denominated in USD

~50% of global debt securities are issued in USD

U.S. Treasuries: largest, deepest, most liquid safe-asset market (~$35 trillion, ~40% of global)

Dollar clearing/settlement dominance (SWIFT, CHIPS, Fedwire)

Economic Foundations

Largest, most liquid capital markets (U.S. ~ 60% of global equities)

Strong institutional credibility and rule of law… at least until recently!

Reserve currency for commodities (oil, metals, etc.)

Deep, flexible money markets and repo system

Global Eurodollar credit system

Behavioral & Strategic Factors

Safe haven in crises

Anchor for global pricing and invoicing

U.S. geopolitical and military influence

Limited alternatives (euro fragmentation; yuan capital controls, etc.)

Given this list, it would take an act of God to remove these guardrails. Accordingly, the recent ~10% decline looks like a normal valuation move, not a prelude to “dollar demise” as the cacophony goes out there. Now, on valuation alone, there could be another ~5% of downside—nothing to get worried about or to spend heavily hedging. For global portfolios, the most effective approach to deal with possible further downside remains: “diversify” --the most effective (and mostly cheapest) risk management tool.

Last but not least: per FactSet/Apollo, ~40%+ of S&P 500 revenues are sourced overseas. Roughly, a 10% decline in the dollar equates to about a ~2% swing in S&P 500 EPS—direction depending on the USD move.

Simon Nocera

San Francisco

Lumen Global Investments LLC